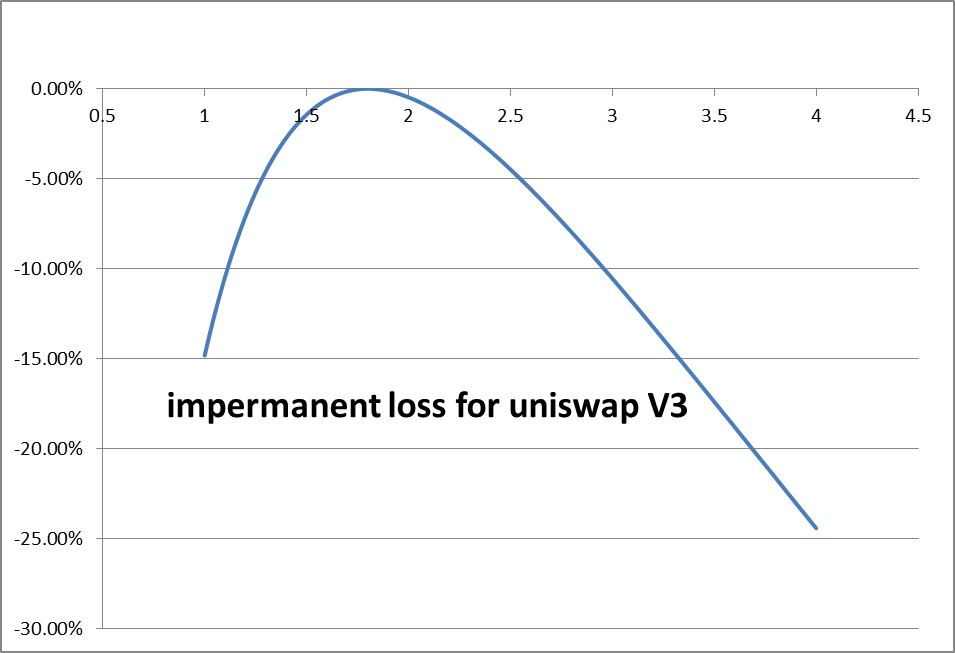

While colleting Liquidity Provider (LP) fees is a pure pleasant process of earning income, by pledging itself a LP’s portfolio value does flatulate along with ETH pricing change. Starting from a 50/50 ETH/USDC holding, when ETH’s price is decreasing, which means most traders are selling ETH, a LP trades against it by buying ETH and eventually ends up with only de-valued ETH on hand; otherwise, when ETH’s price is soaring because most traders are buying it, a LP must sell ETH to the extend that it gives up all its appreciated ETH for USDC. Effectively, a LP scarifies its portfolio value in exchange of LP fees, which could cause huge losses under the sugar-coated fee revenue. Such losses are often referred as “impermanent loss” but could easily be firm and permanent. Therefore, a hedge is required to de-risk such a strategy – Yipingfang is indeed such a hedged LP strategy.

Leave a Reply